In the case, which was heard by the ITAT Delhi bench, Devi Dayal was deputed by her employer – an Indian company engaged in digital technologies – to work on a project in Austria. Both salary and compensation allowance were paid to them by the Indian company abroad. The allowance could be availed by Dayal through a credit card which was valid only in Austria.

During assessment for FY 2016, the IT officer added Rs 21.8 lakh to the taxable income in India because the taxpayer did not submit tax residence certificate (TRC).

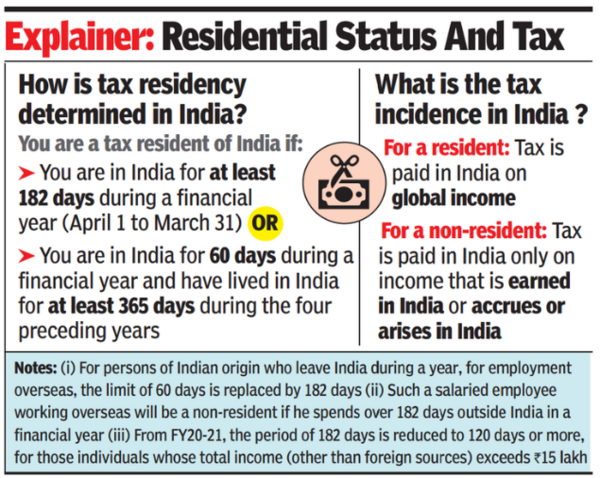

While Indians living abroad are popularly known as NRIs, the nomenclature is different under tax laws. It is not the country of origin, but the number of days of stay in India, that determines whether a person will be resident or non-resident for tax purposes (see table).

Individuals resident in India are taxed on their global income, regardless of where the income is earned. In simple terms, in the case of non-residents, only income that is earned or arises in India (e.g., bank interest from a savings account in India, or rental income from a house in Mumbai) is taxable in the country. is (see table). Thus, salary received by non-residents in a bank account abroad for services rendered outside India is not subject to tax in India.

According to Amarpal Singh-Chaddha, tax partner and India mobility leader at EY-India, “Despite various favorable rulings, there are instances where tax authorities, especially at the lower levels, seek to deny exemption for salaries received outside India. They usually try to do this by not submitting TRC from the host country or not providing proof of taxes paid in the host country, or even received outside India depending on the relationship of the employer and the employee. Challenging the taxability of income, such as litigating the case for various reasons. Employers in India.”

He says that TRC is a mandatory document that is required to be submitted by a non-resident taxpayer who claims any exemption or benefit under the tax treaty between India and the concerned foreign country. This certificate is proof that the taxpayer is a resident of the host country. “In the present case, since exemption was not claimed under the tax treaty, submission of TRC was not mandatory.”

A chartered accountant, who is part of the tax team in a company with global operations, says litigation often arises in split-contract cases, where IT executives seek to tax the portion of the salary that is earned by a company in India. Deposit is made in the bank account. Under split contracts, the employee is transferred to the payroll of the foreign parent company or group company, which pays a basic salary and certain allowances in the foreign country. However, the Indian company deposits a part of the salary into the employee’s bank account in India. This enables the employee to meet certain obligations in India – such as repayment of a housing loan or household expenses (as the family may have in India). Judicial decisions have held that for a non-resident providing services outside India, the portion of salary paid into a bank account in India is also not taxable.